Warsaw’s residential developer housing stock at 2010 levels

High demand for new apartments on the Warsaw residential market resulted in sales increasing by 7% y/y in the Q1 2020. The number of flats coming onto the market for sale was the lowest in six years

Warsaw developers sold 6,900 new flats in Q1 2020, the market’s best result in nearly two years. At the same time, they faced a number of challenges in launching new projects. In the first three months of the year, only 3,700 units were put on the market for sale, down 48% on the last quarter of 2019. Consequently, according to the latest JLL report, at the end of March, only 13,700 flats remained on offer on the capital's primary housing market.

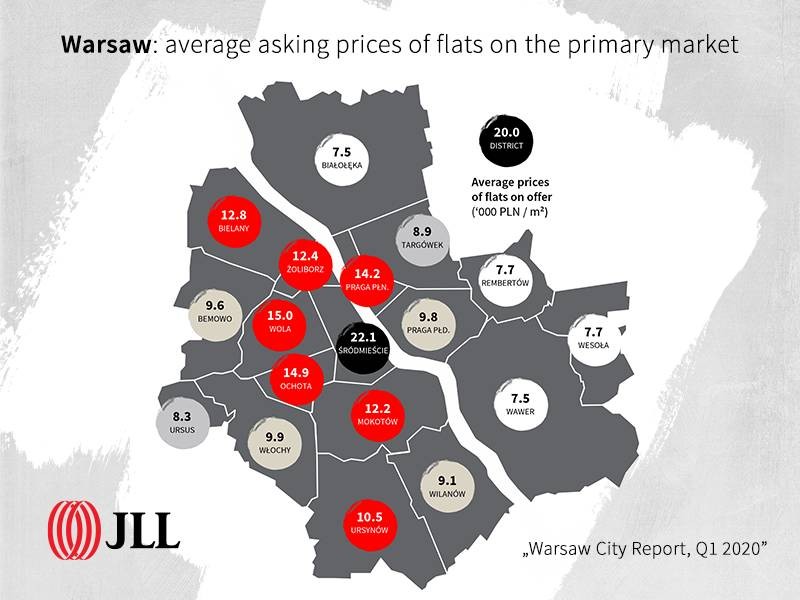

The previously buoyant economic situation that fuelled the optimism of buyers, along with the low interest rate on deposits, and the relatively high availability of mortgage loans underpinned activity in Q1 2020 on the real estate market. Even rising prices did not deter buyers. During the first quarter of this year, prices increased by 3.5% and approached the unprecedented level of PLN 11,000/sqm. In less than two years, the average offer price for units on the primary market increased by 25%, from PLN 8,700/sqm to PLN 10,900/sqm.

As experts point out, the results of the first quarter on the housing market were relatively unaffected by the pandemic, while the halting or significant reduction of the number of transactions experienced in the last two weeks of March and April may, contrary to all appearances, have fewer negative effects on the local market.

“The slow down came at a time when supply was increasingly being squeezed by rising demand. The difficulties experienced by developers in launching new projects, bolder investment purchases along with significant quarterly price increases started to push the market into ‘property bubble’ territory. Fortunately, the prospects of this scenario have receded for the short term. This does not mean that companies operating on the Warsaw market will not face the effects of the pandemic in the coming months but exiting this difficult period may be less challenging due to the lower housing stock levels”, comments Katarzyna Kuniewicz, Head of Residential Research at JLL.

Smaller offer, lower risk

The first effect that JLL experts believe should be expected in the coming months will be the increased number of returns. Buyers who have not yet signed a development contract with a notary - and some of those who chose and reserved a unit in February and March and whose plans were thwarted by the nation-wide lockdown - still have the opportunity to withdraw from these transactions.

“It can be expected that buy-to-let buyers, especially those who are primarily involved in short-term renting, will be first to take advantage of this opportunity. Others may be forced to do so by the policy of banks, which have tightened conditions for granting loans. However, this is still only a fraction of the properties that developers currently have under construction. Although there are more issues related to launching new investments as well as the extremely low housing stock levels on the Warsaw market, this set of circumstances can be offset by the continuing high demand from other groups of buyers, comments Katarzyna Kuniewicz.

What is important for market conditions is the size of the offer in relation to the sales potential and the level of pre-sales, especially in investments at the initial stage of implementation. According to data provided by JLL, the industry’s position looks good. At the end of March, the level of pre-sale in investments that will be commissioned no earlier than a year from the time of the survey was the best since 2008. The Warsaw market, where 53% of units from this type of projects were sold, came out top among the six largest housing markets in Poland. Therefore, we do not predict developers' portfolios being weighed down by a glut of unsold units, as was the case in 2009/10.

“Of course, it cannot be assumed that the future scenario will be similar for all companies operating on the Warsaw market. It depends on the financial condition of individual companies and the strategy of their owners. The situation of these companies will depend on the composition of the portfolio, the financing used by the company, and in particular liabilities such as corporate bonds, cash reserves and availability of equity”, adds Katarzyna Kuniewicz.

“The previous crisis on the housing market taught us that in the first few months, new supply decreases the fastest, followed by demand, and finally prices”.

When will prices start to decline?

“The previous crisis on the housing market taught us that in the first few months, new supply decreases the fastest, followed by demand, and finally prices. However, the expectation that the investments launched by developers for sale in the coming months will be cheaper is not without reason. First of all, newly launched projects can no longer predominantly be targeted at individual investment buyers. This particular group is the first to withdraw from the market. In addition, a change in supply location with increased developer activity in peripheral districts and other locations rather than exceptional opportunities in Wola, Mokotów or Praga should also be expected”, says Katarzyna Kuniewicz.

According to JLL, the remainder of 2020 will see a defence of current price levels combined with discreet discounts, sometimes as part of sales promotions - especially in high-presale investments. Due to the high prices in the first quarter and inactivity in the next, the average asking price of units for the entire year will probably remain at a similar level to that of last year. A more visible price reduction will begin in 2021, mainly due to the launch of new projects of a more economical standard and in less prestigious locations.

More information about the Warsaw housing market and other sectors of the capital's real estate market can be found in the latest JLL report "Warsaw City Report".